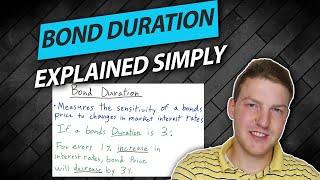

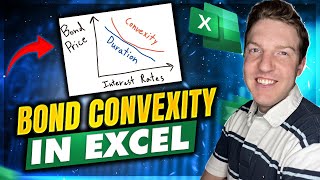

Media Summary: In this insightful tutorial, Ryan O'Connell, CFA, FRM delves deep into the concepts of " Understand how to measure and manage interest rate risk with How to model the sensitivity of a fixed-rate

Bond Duration And Bond Convexity - Detailed Analysis & Overview

In this insightful tutorial, Ryan O'Connell, CFA, FRM delves deep into the concepts of " Understand how to measure and manage interest rate risk with How to model the sensitivity of a fixed-rate